Strategy ONE

Odd-last-period price

Returns the price per $100 face value of a security having an odd (short or long) last period.

Syntax

Oddlprice <Basis> (Settlement, Maturity, LastInterest, CouponRate, YieldRate, Redemption, Frequency)

Where:

Settlement is the settlement date. This is the date, after issue, on which the security is traded.

Maturity is the maturity date. This is the date on which the security expires.

LastInterest is the last date on which interest is accrued.

CouponRate is the annual interest rate of the coupon.

YieldRate is the annual yield.

Redemption is the redemption value per $100 of face value.

Frequency is the number of payments per year. The valid values are 1, 2, and 4 where annual payments =1, semiannual payments =2, and quarterly payments =4.

Basis is a parameter that indicates the time-count basis to be used. The default value for Basis is 0, which is typically used by American agencies and assumes 30-day months and 360-day years (30/360). Possible values for this parameter are listed in the following table.

| Basis value | Application |

|

0 (30/360) |

Assumes 30 days in each month, 360 days in each year. |

|

1 (actual/actual) |

Assumes actual number of days in each month, actual number of days in each year. |

|

2 (actual/360) |

Assumes actual number of days in each month, 360 days in each year. |

|

3 (actual/365) |

Assumes actual number of days in each month, 365 days in each year. |

|

4 (30/60) |

Used by European agencies, assumes the same values as “0” for American institutions. |

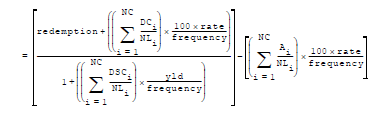

Expression

Where:

Ai is the Number of accrued days for the ith quasi-coupon period within odd period counting forward from last interest date before redemption

DCi is the Number of days counted in each ith quasi-coupon period as delimited by the length of the actual coupon period

NC is the Number of quasi-coupon periods that fit in odd period; if this number contains a fraction, it is raised to the next whole number

NLi is the Normal length in days of the ith quasi-coupon period within odd coupon period

DSCi is the Number of days from settlement (or beginning of quasi-coupon period) to next quasi coupon within odd period (or to maturity date) for each ith quasi-coupon period.

Usage Notes

The Settlement date and the Maturity date should be included within single quotations in the expression for the expression to be considered as a valid expression.